Lovisa - Deep Dive

Lovisa has compounded revenue at 20% for 8yrs (5x), it has 800 stores worldwide and rapidly expanding. I've unpacked my view of the business model and its durability to grow through the next decade.

History of Lovisa

In 2002 a store format was devised by Colette Hayman called Diva Accessories, this store format focused on the “youth” segment of jewellery and hair accessories targeting under 18 year old customers, after 5 years of operating these stores Hayman sold 100% of the store network to BB Retail Capital (Brett Blundy), and went on to create Collette Accessories which grew to 138 stores, then subsequently fell victim to COVID was placed into administration where they were refinanced by an ex Myer executive. The original Diva store format under BB management traded well and rolled out over 100 stores in Australia, see picture below of the Diva and Colette store offering:

In 2010 BB created another brand called Lovisa which was born intending to capture older segments of the market 25-45 year olds. Over the 3 years post the Lovisa brands inception it was clear that Lovisa was the stronger of the two brands generating better unit economics due to its larger demographic and improved product capabilities.

During 2012 BB ran a trial conversion where 21 Diva stores rebranded and converted to Lovisa stores, these saw immediate uplift and traded much better further proving the suspicions of BB that the Lovisa brand was the one to scale. During 2014 the complete conversion took place and the total 88 store Diva network was converted to Lovisa at the same time the business was listed on the ASX at a market cap of $210M with the combined store network generating a forecasted NPAT of $16.6M (12.6x). At the time of the IPO (2014) the Lovisa business had 220 stores in 8 countries, a 20 person product team and over 1300 employees around the world.

Customer

The Lovisa customer is fashion conscious and on trend. Shops for everyday looks, key trends and special occasions. The target market age group is 25-45 years old. The Lovisa product offer encourages quick and easy browsing with frequent store visits without the need to check sizes etc., this makes it an ideal candidate for a “quick fix” for a weekends outfit. On average a customer buys 2.2 items and spends $20 AUD per transaction. This is incredibly low. The customer engagement involves very minimal marketing budget and comprises:

“below the line” advertising which is targeted to the customer not commercial media,

In store marketing with imagery and customer bags, at the IPO this was 1.8% of revenue.

Social Media and digital engagement.

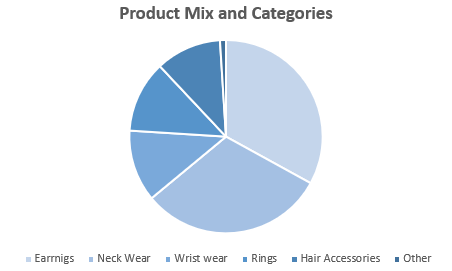

Over 60% of sales are Earrings and Neckwear. Earrings can attract first margins of >86% and Neck Wear can attract first margins of ~83%, first margins relate to sales at full retail price without clearance/discounting. Minimising the gap between first and second margins is critical to profitability (We will dig into this later).

What is surprising is that the product range is globally homogenous with over 90% coverage from Sydney to Botswana (meaning the range is 90% similar no matter where you are in the world). Some ranges attract more demand than others in different markets but customer demand can generally be extrapolated across the world.

Store Economics

The average Lovisa store is located in a AA, A or B grade shopping mall and is 50-80sqm in size. The store is managed with one store manager and flexible support staff. The stores all have standardised fit outs which maintains customer experience but also allows for the use of the same planogram for visual merchandising to maximise sales efficiency throughout the entire network.

At the time of the IPO it cost Lovisa $174k in Australia/New Zealand ‘ANZ’ in Capex and Inventory to open a store and this process took 14 days for fitout and to stock with inventory. Stores are typically refurbished at the end of every lease which in 2015 averaged 5 years. I will drill down on ANZ to un pack some unit economics to highlight how exceptional this business is (Based on FY15):

Average revenue per store: $600,000

Average gross profit per store: $480,000

Average Contribution margin per store: $200,000

contribution is calculated as store gross margin less Occupancy, Labour and other

There are several exceptional observations from this data:

Store sales density is very attractive, using the ANZ store network as the best comparison as its largely matured. Sales per store were $1.02M / 50sqm = $21,200 psqm.

What’s more is that in tracking sales density the sales per sqm in ANZ has grown from $12k psqm in 2015 to now over $21k psqm in FY23, and on a mature store network look through a Lovisa store is trading as efficiently as Lulu Lemon and more than double the sales density of Zara, Uniqlo and Claires. The Average ANZ store now produces greater than $1M of revenue per store.

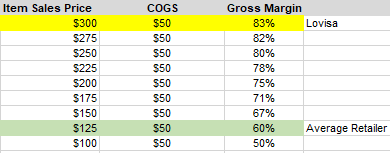

Gross profits per store are very high. The first pass margins on Lovisa product are ~83%, this is before clearance which brings it down to a gross margin level of ~80%. Just to highlight the difficulty in attaining an 80% gross margin I’ve outlined the price mark-up required below. To sell a $50 purchased item for an 80% gross margin you are required to mark it up 6 fold. To move from 60% - 83% is not linear. To attract and maintain such high gross margins requires a strong competitive advantage (I’ve attempted to unpacked my thoughts on this later).

As you can see above the average retailer works on a 2.5x mark up on goods purchased. Normally this mark up is compensated with a high stock turn to generate the returns for the business. For example Costco operates on 14% gross margins but turns its inventory 12.4x a year, this low margin % translates into high margin $ because of the rapid inventory turn. See below as to how Lovisa ranks on this front vs other brands and fast fashion retailers:

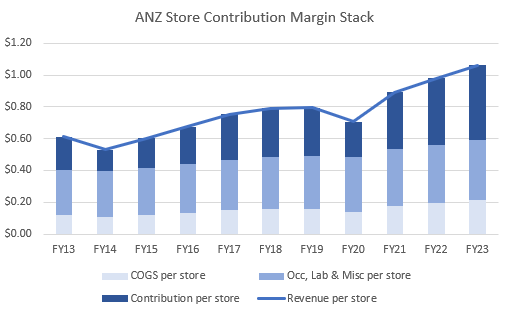

Contribution margin per store is incredibly high. In 2015 an ANZ store was producing 33% contribution margin on ~$600k of sales. Lovisa don’t disclose these metrics now but we can extrapolate from the prospectus to estimate what it could look like with a 3% CAGR in Occupancy, Labour and Misc. costs per store:

This chart shows that in 2015 an ANZ Lovisa store was producing ~$210k of contribution margin, if Labour, occupancy and misc costs are compounded at 3% this contribution per store has grown to an enormous $470k per store. This is because store density has compounded at 6% within the same economic parameters of store size and staffing levels.

The final point about Lovisa is the low capital investment required per store driving a rapid store pay back of ~9 months. An average ANZ store in 2015 cost $124k in Capex to fitout, if we compound this rate at a 3% inflation rate we get to $160k AUD at todays prices, remembering also that ANZ stores are 50sqm so if we gross this up to 80sqm we get to a $260k Northern Hemisphere equivalent. In 2021 the company extended the store fitout timeframe from 2weeks to 2-4weeks, presumably because of the European and USA complexities.

The capex to fit out a store across Europe and the USA is difficult to ascertain as the roll through of refurbishments is not disclosed but given we know that the average lease expiry is ~5years we can possibly assume that 20% of the 2018 store network were refurbished during the year. For a Lovisa store refurbishment costs are typically 1/3 of new store fit out costs. If we add on closed stores during 2023 the business built 210 gross new stores and refurbished 65 old stores (assumptions only). Therefore the net Capex (post landlord contributions) is in the range of $230k - $270k AUD per store. This compares well to others in the USA like Claire’s which are targeting $285k AUD fitout costs for their Mall based 93sqm stores.

Competitive Advantage

Given such attractive margins and unit economics are on offer and given the competitive nature of retailing, why haven’t Lovisa’s margins been competed away? To understand Lovisa’s competitive advantage lets first unpack the business model and how it works.

The Lovisa Business Model

Lovisa is firstly a product company, meaning that the customer offering is highly differentiated and it is the ‘product’ being the jewellery that attracts the customer into the store. This sounds trite but some retailers differentiate their offering based on other factors such as service, price, availability etc. The Lovisa business is referred to as a specialist fast fashion jewellery retailer. But it is also a brand. This brand represents unique pieces of jewellery that are on trend, affordable and broadly available. When a customer thinks of acquiring a piece of jewellery for an event they think of Lovisa.

The Lovisa fast fashion jewellery model works by following innovators not being one, the internal design teams capability is focused on re-creating not creating. This is not an easy capability to develop. It takes lots of experience, training, focus and resources to build a team of buyers who can successfully identify the fashion forward people to follow and styles to re-create. It also takes a disciplined business model to take this product from early adopter to early majority before moving on when it becomes mainstream and margins become compressed, see below.

Typically innovation and rapid distribution of product capabilities are not found together, normally a business is one or the other. It is the combination of the two that creates the strength in the business model.

Lovisa’s has an inhouse design team of 20+ specialist jewellery designers that focus solely on identifying fabrics, materials and designs at worldwide trade fairs, fashion shows, social media, magazines and any source of on trend influence. This team then put together an inspiration board including all newly identified trends, from this they identify 3rd party manufacturers where samples are inspected by Lovisa staff before being ordered in volume for the global network, this process is very fast and takes 8-10 weeks from concept to store shelf. And Lovisa are very good at this process, producing over 100 new products every week. What is critical about for the profitability in this part of the process is the inventory management. Lovisa have customer feedback loops linked to their store network via their daily sales records which trigger a re-ordering pattern if a new item is successful it an be expanded with a larger fixture. If a new product sells well in its first few weeks of trade it can be re-supplied within a 4-6week window. The trick is maximising the opportunity while getting off the trend before it rolls over and becomes an item that needs discounting or ‘clearance’. It is this speed to market and continual exploitation of this window of the trend that allows for the gross margins of 80%.

From the outside this appears simple, you get on trend jewellery and you sell it through stores in good locations. However, executing the synchronisation of the dozens of different little things is not easy to manage, especially across 800+ stores in 39 countries.

In summary the business model works by:

Targeting affordable price points (A$6.99 - A$49.99)

Sourcing on-trend product and making it available on mass at short lead times

Responding to trends rather than trying to predict or create them

Building hardened supply chain systems to respond and deliver product with great control over quality and quantity

Constant release schedule of new product which acts as a form of advertising encouraging repeat store visits and increased spend due to scarcity

Small batch sizes and inventory management to limit large clearance activity and enhance gross margins

Industry Structure

I will just briefly unpack the 5 elements of the industry to look at the competitive dynamics of the industry first.

Suppliers

The bill of material of a piece of jewellery is mainly raw material and labour. In the key supplying regions for Jewellery (Asia) Raw material is abundant and so is labour this has resulted in the development of hundreds of wholesale jewellery manufacturers. In China most of the wholesale manufacturers are based in Qingdao, Yiwu, Guangzhou, and Shenzhen. Due to the number of large manufacturers and ease of air freight shipping due to the size and weight of the product switching between suppliers is also relatively easy. As a result of this suppliers have low bargaining power

Substitutes

A substitute to wearing fast fashion jewellery could be the acquisition of higher quality pieces, purchase of pre-loved jewellery or even making custom pieces these are all not easy substitutes as they are not readily available, and don’t meet the desires of the customers (being on trend, affordable and readily available). Both of these are possible at the fringes of demand but at the broad majority. Threat of Substitution is low.

Buyers

If the average transaction value is $40 AUD Lovisa has completed 15M transactions in 2023. These purchase prices are so small and the spread of customers is so large that no single buyer has sufficient weight to demand special terms or conditions. Buyers have low bargaining power

Potential Entrants

If you were to look at the below image you might be encouraged by the opportunity. It appears from a lay person that the same earrings that are sold in China for $2 AUD are sold in Lovisa for $18AUD.

It also seems that given the minimal capital outlay required to lease a physical store, spin up an online shop front and hire some fashionable people there are low barriers to entry from economies of scale. However, The experience curve is the key barrier to entry in my view. This barrier is tendency for unit costs to decline as a firm gains cumulative experience in producing a product. Fast Fashion Jewellery retailing has several specialised business processes including Designing, Procurement, Logistics, Inventory management, retailing, property management/negotiation, labour management, sales, merchandising etc that have been developed by Lovisa to maintain superior economics. It is not cost prohibitive to compete but it is difficult to compete at the same profitability. This is illustrated by the large number of insolvencies in this sector. I consider there to be moderate threat of new entrants.

Industry Competition

The fast fashion jewellery offering sits in a unique position in the market:

The affordable jewellery offering is limited across all three major retail types, often the jewellery departments are also managed by third parties and managed by concession not by range. As you move across to Department stores and accessory retailers the range deepens slightly but it is not the primary focus, as we have discussed above by not being at the right point of the trend all the time you erode margins. The rivalry among these competitors is low given there is significant diversity among the landscape with almost all sources of competition having different inventory and business focus. In Lovisa you might find a directly comparable product that you can compare prices but if you do there are 100 additional new products hitting the shelves that week. I consider there to be moderate rivalry among existing firms.

In summary, over all I believe the key structural features of the fast fashion Jewellery industry to have Low-Moderate strength meaning that the Lovisa business unit will be able to find an area of the jewellery industry to produce sustainable profitability through defending itself with multiple Buyers and Suppliers, Low level of substitute products, long experience curve extending the product differentiation for new entrants and moderate internal rivalry from current industry.

Long Term Opportunity

The way I think about LOVs long term potential is on a store footprint basis combined with an escalating contribution per store as sales density increases like it has in ANZ.

Global Store Footprint

I believe in 10yrs LOV could have 3,000+ stores worldwide, this is an additional 240 stores per annum from today. Is this gross build capacity possible? To unpack the requirements for this I believe there are a few key considerations:

1- The store closure rate historically in the Lovisa network has been ~4% pa (in FY23 they closed 37 stores)

2- The store refurbishment rate is 20% of 5yr prior network.

This means that on average the property team needs to be opening 309 gross stores per annum (397 at peak) incorporating an average closure rate of 68 stores a year (107 at peak) AND refurbishing 180 stores per annum (332 at peak). Sometimes a site is closed and then re-opened again some years later when the landlord waives lease increases. however this means the team will need to be building an average of 489 stores each year and at the peak year in 2032 this will be 730 stores. To achieve this target there are a few important things one being the volume of AA, A and B grade retail space required, the second being the number of individual locations. These are two very difficult elements to study without industry knowledge, I have done my best at this below.

I have broken the 3,000 store target up into the key regions to firstly see if the key markets handle their share of the footprint. In my mind there needs to be ~1,000 stores in Europe, ~1,000 stores in Americas and ~1,000 stores in Asia/Africa. I’ve unpacked these markets below:

Americas

In the USA market there are 1,220 super regional and regional centres, these are large Malls with >600,000 sqft of retail space with >40-80 stores each. We need to be careful we aren’t undercooking the long term TAM here though because there are a further 10,000 large neighbourhood centres (15-40 stores) and a further 100,000 Strip Malls/Small neighbourhood centres. In my experience good managers continue to expand their TAM far beyond your original expectations (Dominos Pizza did this so to did Starbucks, Analysts continually chided Sam Walton about his TAM running out). I feel comfortable that the capacity is there to handle 1000+ LOV stores. To look at some precedents of other retailers who have tested this theoretical limit I lean on Claire’s which has ~2000 stores in the USA and Canada of similar size (93sqm) selling the same type of product.

Europe

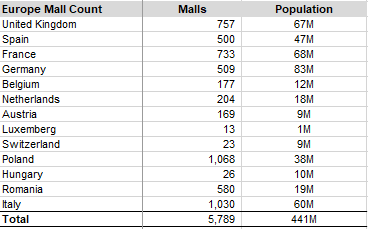

The European market is harder to dig into however just focusing on the countries Lovisa are currently in I’ve tried to research the total number of Shopping centres (Malls) in each geography:

This well and truly covers the 1,000 store capacity. And to look at a precedent in these markets I have looked at Claires again which has 871 stores across Europe but I have also looked at Zara and H&M both which are more European centric retailers. These two brands have ~2,000 stores each in Europe currently (remembering that the average Zara/H&M store is 30,000 sqft (30x larger than LOV).

Asia/Africa

The size of some of these countries and markets in Asia are crazy. For example greater China alone is estimated to have 4,600 shopping malls (4 times the US market size) and accounts for half the malls built worldwide! The China economy is also expecting to open a further 7,000 malls over the next seven years. In India there are estimated to be 2,000 shopping malls and is expected to grow by 50% in the next several years. There are also very strong examples inside both of these markets of jewellery retailing success. In China Chow Tai Fook Jewellery has 7,269 stores selling high end jewellery with an ASP of $2,955, There are also other examples at the affordable mass market end of the market. For example Miniso has 3,226 stores in Mainland China selling discount accessories at an ASP of $2.55. Another example I could find in China was Peacebird accessories which has close to 5,000 stores selling low priced clothing. In India the best store network I could find was Titan Company Ltd which is part of the Tata group, it has 1,300 stores across India and produced $4.7B of revenue with 80% of its sales in Jewellery. It claims to only have 6% market share.

All of the above examples in Asia are by no means comparisons to Lovisa as they are very different and these markets are insanely difficult, borderline no go zones in my view (I’m a sceptic on growth in China) however I included them to highlight the scale of these markets. I think the Asian growth will come from a number of countries not just Mainland China and India. To look at a precedent of a western company that has scaled in both these countries I again look to Zara (which segues nicely into my next section on Management), Zara have 28% of their store network in Asia. Lovisa already have 250 stores in Asia so in my model I have modest 130 store networks for China and India in 2032 and most of the growth from S.E Asia and Africa.

Management

Although this deep dive is attempted to be focused on the business, bulk of the long term conviction comes from capital allocation, focus and discipline. By being lazy I normally focus on the protection of share count (not issuing capital), insider ownership, related party transactions and Incentives to score management. I will briefly outline each of these below but also introduce Victor Herrero the current CEO. Victor Herero replaced long standing and founding CEO Shane Fallscheer only two years ago. Shane was the CEO of Diva and led the IPO and the store growth to ~500 stores including USA and UK markets.

Victor Herrero

Victor’s most exciting experience is his tenure with Inditex (Zara) starting with them in 2003 until 2015 with the last 3 years spent as Managing director of China where they rolled out a multi hundred store network. Brett explained when he was announcing the replacement - in my words - he is a ‘get shit done’ person who accepted no excuses or barriers to achieving his objective. He is a true citizen of the world speaking 6 languages and spending 250 days a year travelling to new markets. I have heard stories that he travels with no suitcase and minimal luggage finding a Zara store at his new destination to buy a new suit and discard his old one and keep going. I have also heard stories of him ripping through existing stores speaking into his iPhone recorder to shoot his team a voice memo before rushing off to new store visits. He seems to me to be a true fanatic!

Share count

Lovisa have been very good with shares on issue. At the IPO there were 105M shares on issue and now there are 107.7M only growing 0.3% CAGR over 8 years. I have forecast this to grow to 112M in 2032 as the CEO Victor Herero’s LTIP is paid out over the next 3 years plus any more in the future.

Insider ownership

The insider ownership at Lovisa is very high with founder Brett Blundy owning 40% of the business. He is very engaged and active as the Chairman. I know that he still runs certain senior management events and attends some strategy sessions with senior leaders. I also understand that when there are key strategic opportunities on the table he is in the trenches executing the deal. For example in COVID Lovisa acquired a large store network in Europe called Beeline GmbH. This deal was exceptional with LOV being paid 10M Euro to take over the network of stores, my understanding is that Brett travelled to each of the 144 stores in the Beeline group to do his own personal DD. I also understand that this is by far his largest investment, currently valued at $900M AUD. He hasn’t sold a share since the IPO. Brett also pays himself a Chairman fee of $150k with a further $81k paid as a reimbursement of costs to his entity BB capital.

Related Party Transactions

There are zero related party transactions other than the reimbursement of costs and his directors fee. Also worth noting that he doesn’t participate in any LTIP plans himself and has never taken options or large share based compensation etc.

Incentives

The LTIP plan is very aggressive but aligned to shareholders, and I must say its refreshing to see this rather than a typical relative TSR hurdle consultant/box ticking plan.

The current plans works as follows:

Tranche 1 - FY23 - 100% vested but required 30% growth in EBIT, Victor achieved 87% of this as the business grew EBIT at 26%. For this achievement he was granted 347,671 shares. This is the smallest tranche of the plan.

Tranche 2 - FY24 - to achieve 100% of this year he must achieve EBIT (Pre the expensing of this plan through the P&L) of $130M. For this achievement he will be granted 1.7M LOV shares.

Tranche 3 - FY25 to achieve 100% of this year he must achieve EBIT (pre expensing of the plan) of $155M. For this achievement he will be granted 1.2m LOV shares.

For Victor to achieve this I estimate the business will need an end of year store count of 1,200 stores, LFL sales growth of 3% across all regions (except Asia) and the same cost structure as FY23.

There are two very favourable outcomes from this plan, firstly, Victor will be more incentivised to grow Lovisa post this award as compounding his LOV holding pre-tax is worth far more than jumping ship for another incentive plan somewhere else. And two he is going to be a quasi owner with a ~$100M holding which will hopefully result in lower incentive plans moving forward and a long term focused management team.

Valuation

I have an ~18% IRR on Lovisa at a $2.3B market cap (~$21 per share). This is based off store count growing to 3,017 stores by 2032 with a 17% NPAT margin exiting on a 22x NPAT multiple and an 80% Dividend pay out ratio (high I know but due to the capital light nature of the business previously it has been 100%!)

A 22x NPAT multiple seem reasonable when compared to more mature fast fashion retailers like Zara and H&M that are both on 24x and 27x respectively and if you want to get a bit more bullish about the brand element to Lovisa, Lulu Lemon is trading on 33x NPAT. Please contact me if you are keen to grab my model and use it for your own estimates.

I hope you found this worthwhile, please reach out if you would like to discuss.

Nice detailed insights, was a buyer on the recent pullback on ceo change, i tend to think with lovisa’s economics the CEO running the show isn’t necessarily a huge factor especially with their growth opportunities, also, Brett is still at the helm and as you said he still takes the shots where it matters for the firm.

I’ve enjoyed your write ups! If you’re in Sydney, would be pleased to grab a coffee some time, always enjoy meeting like minded investors. - Damon from ECP Asset Mgmt.